Are you drowning in inventory management complexity? A periodic inventory system—which involves updating inventory records at scheduled intervals rather than in real time—could save you time, money, and headaches.

In this article, you’ll discover…

- How periodic inventory systems work and their key benefits

- Calculating inventory using the periodic method

- Best practices for implementation and overcoming common challenges

- How to determine if this system is right for your business

Let’s dive in and unlock the potential of periodic inventory systems.

How does the periodic inventory system work?

A periodic inventory system is an inventory management method in which businesses update their inventory records at scheduled intervals rather than in real time. It involves physically counting stock and reconciling books at set periods (e.g., monthly, quarterly, or annually) to determine inventory levels, calculate the cost of goods sold, and identify discrepancies between recorded and actual stock levels.

While some businesses choose to update their costs, beginning inventory levels, and ending inventory levels frequently, you might not require real-time updates on this information.

Before you decide if periodic inventory works for you, there are a few important characteristics to consider.

Tied to your accounting period

Using a periodic inventory system can help you align your inventory records with financial reporting. Rather than relying on potentially pricey, complex inventory management software that provides real-time updates, you’ll monitor your inventory at intervals throughout the year, such as monthly, quarterly, or annually.

Relies on an accurate physical inventory count

Any mistakes made during the inventory audit and counting process will result in discrepancies between your recorded inventory purchases and your actual inventory. As a result, if your team doesn’t handle the physical inventory count carefully, you can develop errors in your ending inventory calculations and cost of goods sold.

Ideal for low-turnover or low-value inventory

If many of your products are infrequently sold or do not have to be restocked often, or if you’re a small- to mid-sized ecommerce business with low-value inventory items or small inventories, the periodic inventory system will be a practical and effective choice. Since it involves a physical inventory count, it’s not well-suited to vast amounts of inventory that’s rapidly changing.

Does not involve real-time data

Unlike other inventory systems, this method doesn’t implement real-time tracking inventory technology. Therefore, it creates a gap between counting sessions where your business will not have updated stock information.

How do you calculate periodic inventory?

Periodic inventory is an accounting method wherein businesses update their inventory records at set intervals, typically at the end of an accounting period. While the method itself is not a formula, there are several specific calculations associated with it that involve determining the cost of goods sold (COGS) and the ending inventory at the end of an accounting period.

The calculation processes associated with this system are straightforward and—most importantly—they will allow you to conduct easier counts, simplify your record keeping and give a clear snapshot of inventory value.

Step 1: Calculate the cost of goods sold (COGS)

Sometimes referred to as COGS, the cost of goods sold is a term that refers to all of the expenses involved in obtaining the products you sell.

This includes:

- Raw materials

- Direct labor

- Manufacturing overhead costs

- Shipping and handling costs

- Storage costs

- Packaging materials

- Cost of purchased components or subassemblies

- Royalties or licensing fees related to production

- Inventory write-offs or adjustments

Understanding how much money you’re spending to produce the items you sell is critical for remaining profitable. Once you understand the cost of the goods you sell, you can set prices that cover your expenses and understand when it’s time to improve your profitability.

The COGS formula

In a periodic inventory system, the first step in calculating your COGS is to physically count your in-stock items and then determine the value of your inventory.

Next, you’ll need to refer back to the value of the inventory that you had in stock at the beginning of the accounting period.

Finally, you’ll need to review how many inventory purchases you have made since the accounting period began. With this information, you can calculate your COGS with the following formula:

COGS = Beginning inventory + Inventory Purchases – Ending Inventory

If you have these figures handy, this calculator will do the work for you:

Cost of Goods Sold (COGS) Calculator

Your accounting period can be any length of time that you desire, and you can always use your remaining stock from your previous accounting period as your beginning inventory. At the end of your accounting period, you’ll update your ending inventory balance and transfer your COGS to an income statement for future tax purposes.

Step 2: Determine your ending inventory

When calculating your cost of goods sold, determine the value of your beginning and ending inventory.

There are several methods you can use to accomplish this, depending on your financial reporting goals and business objectives.

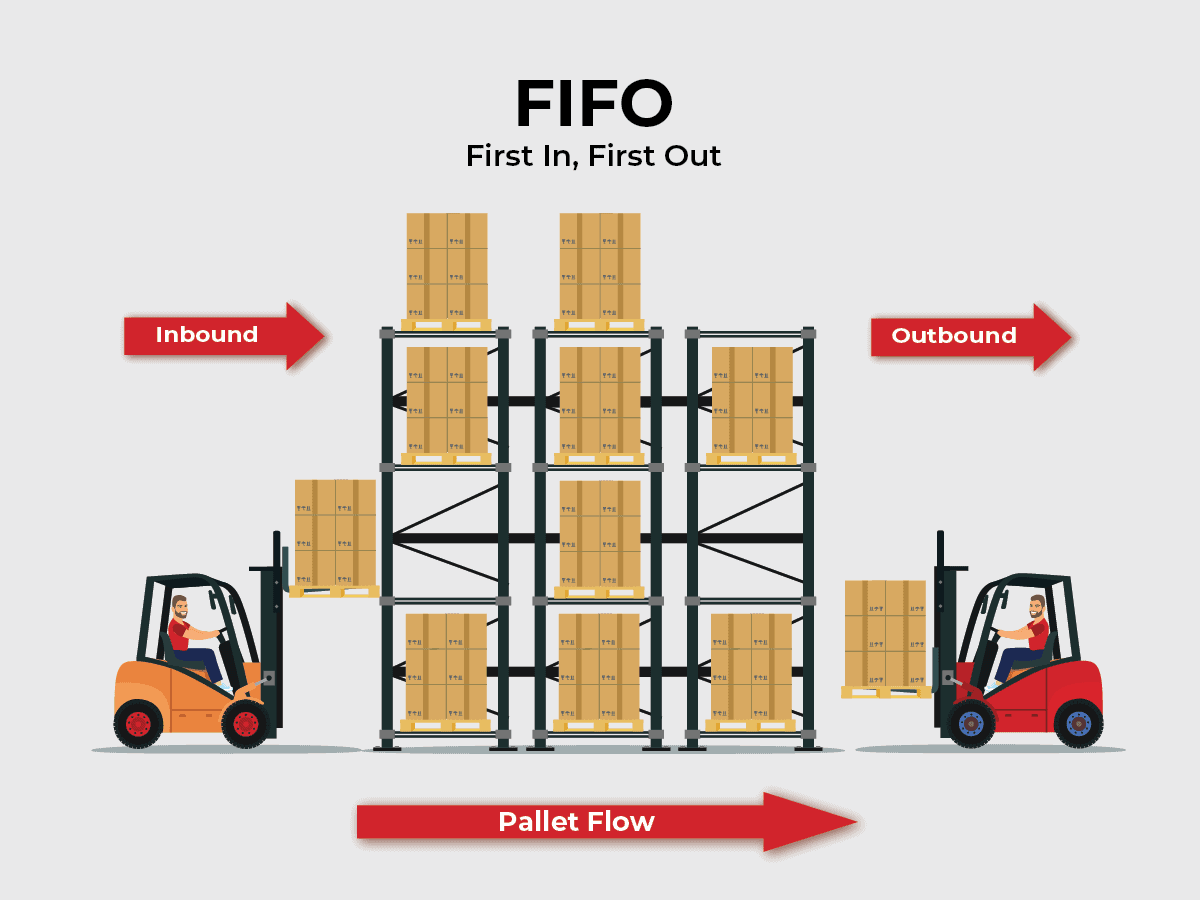

The first-in, first-out method (FIFO)

This inventory valuation method assumes that your oldest assets will be the first sold. When you use this method, your cost of goods sold will be based on the cost of your oldest inventory purchases multiplied by how much of that inventory you sold. During periods of inflation, this method results in lower COGS, a higher ending inventory value and higher reported profits.

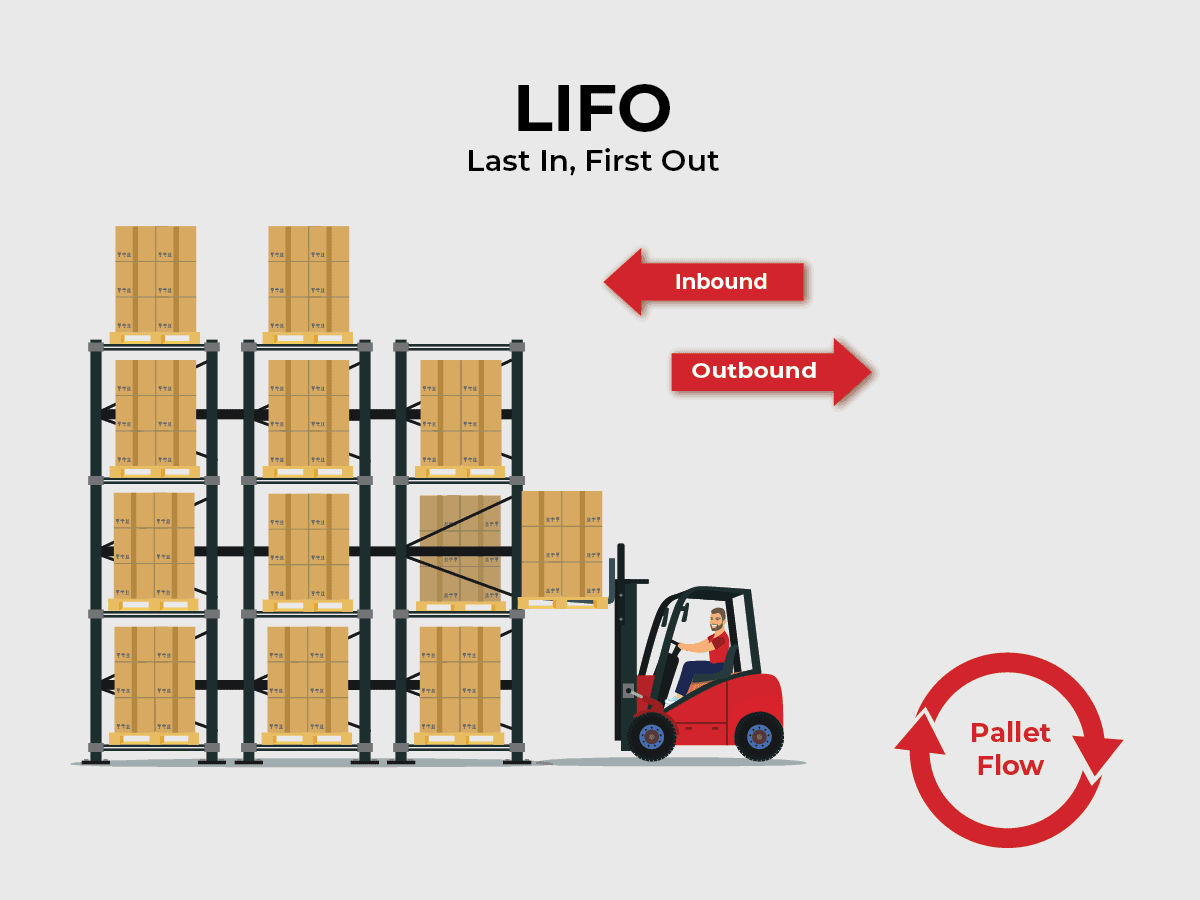

The last in, first out method (LIFO)

This method assumes that the last items you purchase will be the first sold. With this valuation method, your COGS is based on your most recent inventory purchases, and your ending inventory will be valued at the cost of older inventory purchases.

Last-in, last-out can result in higher COGS and lower ending inventory values during times of inflation, because the more recent and more expensive inventory is considered sold first. This can result in lower reported profits for your business.

NOTE: LIFO is not allowed under International Financial Reporting Standards (IFRS).

The weighted average cost (WAC) method

Using this valuation technique, you will calculate the average cost of all of your inventory items that were available during the accounting period. This average cost will be applied to your units sold and units remaining in your inventory.

This method aims to reduce drastic price fluctuations, resulting in COGS that fall between the results of FIFO and LIFO. An average weighted cost method can be a good option if your business features inventory items that are very similar.

Periodic inventory FAQs: What are the periodic inventory system advantages?

For smaller companies that don’t require a highly detailed or easily scalable inventory system, the periodic method is effective and beneficial. If you implement this system, you can expect a quick and easy adjustment period, with minimal cost investment.

Fast and easy to implement

Periodic checking involves fewer records than other valuation methods and is often faster to calculate. Since you’ll only have to count your inventory at a few designated times throughout the year, you’ll save a lot of time. This is a significant advantage if your business is new or has limited resources.

Requires minimal information

Unlike a perpetual inventory system that requires highly detailed information on each sale and purchase (more about the perpetual inventory system below), periodic systems don’t require you to monitor each transaction.

Keeps costs low

Since you only need to perform a physical inventory count, you won’t need to purchase any additional equipment or new digital tools.

Requires minimal staff training

Even though physically counting your inventory is time-consuming, it’s easy to perform. If your business is experiencing high turnover rates, it will be particularly beneficial to not have to train staff on complicated software products.

An alternative: perpetual inventory system

An alternative to the periodic inventory system is the perpetual inventory system.

The perpetual inventory method involves continuously monitoring your business’s inventory balance. After each sale, your inventory balance will be automatically updated using technology like supply chain management software, RFID readers and point-of-sales systems.

Which inventory system should your business use?

If you’re not sure which system to use, use this comparison table to help you make a decision.

| Factor | Periodic System | Perpetual System |

|---|---|---|

| Accuracy | Less accurate between counting periods. Prone to discrepancies due to less frequent updates. | High accuracy with real-time updates. Provides up-to-date inventory levels at all times. |

| Inventory Complexity | Suitable for limited products and simple inventories | Better for large, diverse inventories |

| Real-time Tracking | Minimal data between counting periods | Provides real-time tracking |

| Ease of Use | Simpler to implement and use. Requires less technology and can be managed with basic tools. | More complex to set up and use. Requires specialized software and training. |

| Staff Training | Requires less training; beneficial for high staff turnover | Requires more extensive training and investment |

| Human Error | More prone to human error | Can reduce human error through automation |

| Financial Information | Offers minimal data between counting periods; may require large adjustments at end of accounting period | Provides up-to-date financial information |

| Inventory Turnover | May not be suitable for dynamic inventory turnover | Immediately alerts when items are sold out or overstocked |

| Implementation | Simple to implement and manage | More complex to implement but offers advanced functionality |

| Cost | Lower initial cost. More cost-effective for smaller businesses or those with simple inventory needs. | Higher initial cost due to technology investment. Can be more cost-effective long-term for large inventories. |

| Suitability | Best for small businesses with simple inventory needs and slower inventory turnover | Ideal for businesses with large inventories, high-volume sales, and complex multi-channel operations |

Improve your inventory management with Red Stag Fulfillment

Effective inventory planning is crucial for ecommerce success, but it’s also one of the biggest challenges businesses face.

That’s where Red Stag Fulfillment’s inventory planning service can help. We’ll help you balance stock levels to meet demand without tying up excess capital, using tools like demand forecasting and real-time inventory data through our online dashboard.

But when you partner with Red Stag, you’re not just getting inventory management—you’re outsourcing your entire ecommerce fulfillment process to experts. We handle everything from receiving and storing to picking, packing, and shipping. Our zero-shrinkage guarantee and strategically located warehouses help optimize your inventory turnover and reduce fulfillment costs.

Ready to stop worrying about inventory management and fulfillment? Contact us today to see how outsourcing to our award-winning 3PL services can free up your time and resources, allowing you to focus on growing your ecommerce business.